Our Services

Annuities

Basic Introduction To Annuities

Few financial tools have experienced the meteoric rise in popularity as annuities have. In the last 10 years, the utilization of annuities has skyrocketed as more and more aging baby boomers choose these products as stable vehicles to protect their assets and provide reliable income in retirement. If you’re over the age of 50, you’ve surely seen articles, advertisements and educational events promoting these innovative tools. But you probably have some questions: How do annuities protect my money? Are annuities safe? Will I pay taxes on assets inside an annuity? How accessible is my money in an annuity?

As an expert in the field of annuities, I encounter these questions and many others on a daily basis. The purpose of this page is to shed light on some of the benefits of annuities in an effort to give you an accurate representation of fixed annuities and to answer some of the basic questions many people have.

College Planning

College and Retirement – You Can Do BOTH!

For many families with growing children, there is a challenge to achieve multiple financial goals at the same time. Particularly saving for retirement while planning for college. The road to college is not without its challenges, but with proper guidance, I can show you how you can achieve both of your goals at the same time.

Here’s how I help my clients with college planning:

Approximately 70% of applications have errors that result in lost potential aid. As a college planning expert, I can guide you down the correct path to capture the maximum aid possible.

Building a retirement plan and a college plan must be coordinated. The way you save for retirement can often-times have a negative impact on your children’s aid opportunities. I can help you skillfully manage both retirement and college planning. Once your children are in college, you need a partner to guide you through the college years while still building for retirement. Little-known creative financial planning strategies can not only help for retirement and college planning, they can make a dramatic tax difference for you throughout your lifetime.

If you are facing the challenge of preparing for college, you need expert guidance to maximize both aid opportunities and your future retirement. Call my office and request a complimentary college planning consultation. Taking the time to plan may very well save you and your family greatly in the future.

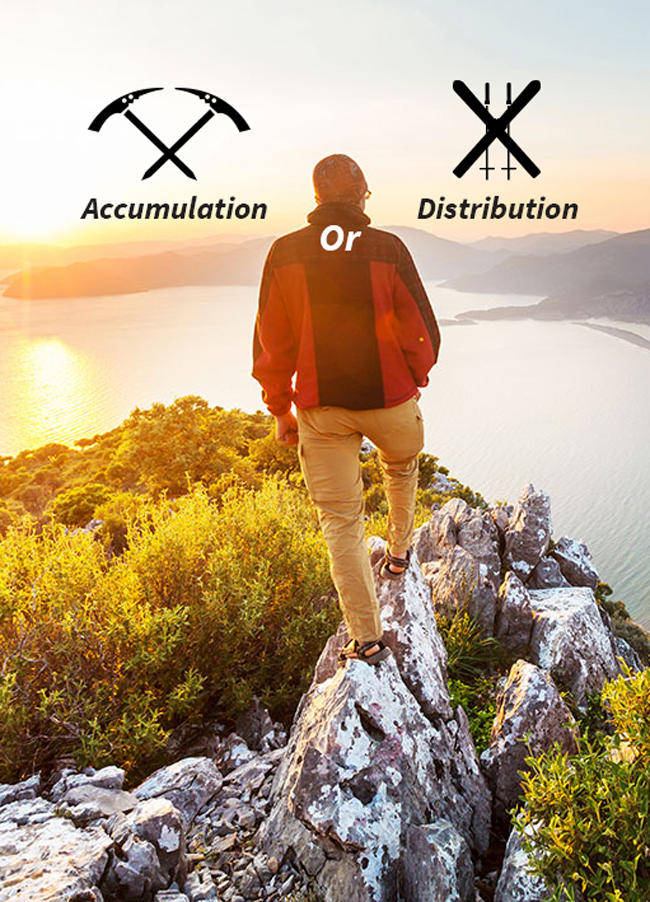

Income Planning

As the slope turns downward the tools that we used to climb the mountain are no longer useful. To descend the mountain we need a new set of tools, so we trade in our ice picks and ropes for skis and ski poles. When retirees attempt to use financial tools designed for growth and accumulation to generate an income, the results can be disastrous.

Dr. Marshall Goldsmith is famous for saying, “What got you here won’t get you there.” The processes we have developed can help you determine where you are on the income planning mountain and develop a plan to help protect and preserve your retirement savings. Your specific circumstance is unlike that of any other person. We realize this and custom design all our solutions specifically for the needs of each client. When it comes time to distribute retirement income, we’ll show you strategies that can help ensure that your savings can last throughout your retirement years. With appropriate planning, 21st Century Financial Services can help you attain a more secure quality of life throughout your retirement.

Life Insurance Planning

Sleep better at night with the peace of mind knowing that your loved ones will be taken care when you are no longer there to provide for them. A good life insurance plan could be the only thing that stands between struggle and stability for those you leave behind.

Why Do I Need Life Insurance?

The most basic answer is this – security. But there are many benefits to a good life insurance policy beyond the assurance that comes with knowing your family won’t be burdened with costly funeral and medical expenses after you’re gone.

When you think about the future, what comes to mind? Maybe the long-term financial security of your loved ones is your top concern. A good life insurance policy can replace your earning power to provide that continued stability. Do you need a safety net in place for financial emergencies? Are you worried that your current savings won’t be enough for retirement? Maybe you want the freedom to invest or help cover tuition costs when your kids go to college.

Whatever concerns or goals you may have, a quality life insurance policy could be the solution. 21st Century Financial Services has a team of expert agents who can answer all of your questions.

What Type of Coverage Do I Need?

As an individual, you need a life insurance plan that matches your individual needs and goals. There are multiple options available and finding the right one can be tricky. Before meeting with one of our agents, take a minute to look over the two main categories of coverage.

Retirement Planning

In these unprecedented times, we must make sound financial decisions based on the things that we know. At 21st Century Financial Services we know that when the financial landscape changes, the tools we use must change to remain relevant. We know that while the world of finance is filled with compromises, our client’s goals can never be compromised. Above all else, we know that our clients and our business will continue to succeed so long as we embody our three core values; wisdom, empathy, and experience.

Social Security

Claiming your Social Security benefits is one of the most important retirement choices you will ever make. However, it may surprise you to learn that 77% of financial professionals do not talk to their clients about strategies to maximize the benefits their clients will receive from Social Security. Making matters worse, the Social Security Administration prohibits their employees from giving detailed claiming advice. Because some very simple planning can increase your benefit by 67%, we have dedicated ourselves to educating our clients about this important decision. We use industry leading software to show you not only when the best time to claim your benefit is but also how you may be able to take advantage of little-known strategies that can further increase your benefit.

Social Security is a valuable asset and should be managed as such. For many people, this will mean using any number of social security maximization strategies. Although every individual will present a unique set of goals and financial constraints, it many cases it will pay off to delay taking Social Security benefits if possible. Because what will work best for you will ultimately depend on your specific financial situation, it is best to work with a financial advisor that has knowledge and expertise in this area of retirement planning.

The planning process that we use with our clients helps to answer the following questions:

- How is my benefit determined and at what age should I apply?

- How can I maximize the benefit and make it meaningful based on my objectives?

- What happens if I wait to take it after full retirement age and what are the pros and cons of doing so?

- How can social security provide the most for my spouse in life and at my death?

- What about COLA's, divorced spouse benefits and survivor benefits?

- How will continuing to work after I began taking benefits affect my benefit and how will benefits affect income taxes?

- How can I best coordinate social security with other retirement income sources?

- When does it make sense to delay taking benefits?

- What are innovative strategies for maximizing benefits with my spouse?

- To find out if something is missing in your current financial planning call us today.